Unlock the Editor’s Digest for free

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

To mark the event of the bankruptcy of WeWork, Morgan Stanley has published a multi-region survey on offices. No surprise that everyone still hates them, though no one hates them more than the Brits.

Post pandemic the UK leads the table for work-from-home days taken, having been the most office-bound workforce before 2020. The British are also the most ambitious when wanting more time at home:

The sample is of 4,126 working-age respondents in the US, UK, Germany and France. More than a quarter of Brits and Americans said they would quit their jobs if forced to back to the office five days a week . . .

. . . and they’re generally the least prepared to suffer a long commute to appease the boss’s presenteeism:

A majority in all regions choose to reinvest the commute time saved doing literally nothing:

Bosses say they want full attendance. KPMG’s 2023 survey of 1,300 global CEOs found that 64 per cent expected a full return to the office within three years, and 87 per cent said they would be rewarding those who turn up with favourable assignments, raises or promotions.

But employees either don’t believe them, or don’t care:

And unsurprisingly, across all geographies, it’s the wealthy and the young who are rejecting office life …

. . . though the boomers are just as disaffected as Gen Z. Nearly half would prefer to be in the office one day per week or less.

So of course, their employers have been . . . adding office space?

Weird. Maybe the buildings just look bigger when there’s no one in them? Whichever way, Morgan Stanley concludes that the prime property Reits will probably be fine.

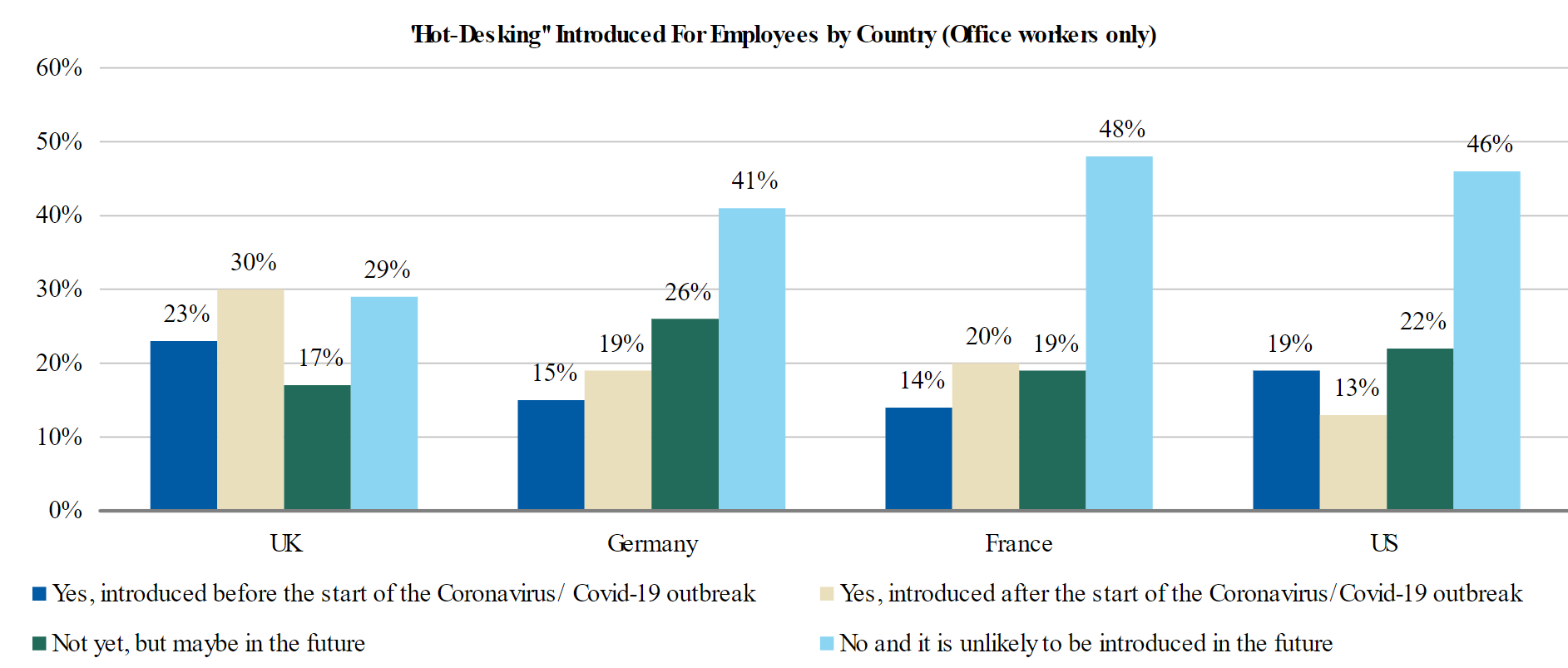

Vacancies have been a problem in “periphery locations” like Canary Wharf in London and La Défense in Paris. But it’s not a crisis for as long as employers go easy with hot-desking, and the landlord can put an eco-friendly claim in the brochure for its centrally located refit.

So even if WFH can’t be undone it’s probably more than in the price for UK Reits, says Morgan Stanley. They were more scarred by the 2008 financial crisis than continental peers so have been more disciplined with leverage.

Its team also notes that European landlords can lack transparency, with more use of off-balance-sheet debt and hybrid instruments that are booked as equity.

The broker’s scatter chart has London-focused operators Great Portland Estates and Derwent London as running the most conservative balance sheets while offering implied yields that are average to good:

Derwent and Great Portland both trade about 38 per cent below net asset value, against a UK sector average of 21 per cent. The deep discounts reflect expectations of more valuation markdowns of London prime property, but also the possibility that they will tap shareholders for acquisition firepower as soon as the office market shows any sign of an upturn.

Going by Morgan Stanley’s survey, that day could be very far away.

{kind=link}