Unlock the Editor’s Digest for free

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

The core US inflation rate has now fallen back to its lowest since April 2021. Huzzah! But if it hadn’t been for Republican scepticism it might already have been back near the Federal Reserve’s 2 per cent target by now.

At least, that’s the intriguing suggestion of a new paper written by Carola Binder, Rupal Kamdar and Jane Ryngaert and published by the National Bureau of Economic Research this month.

MainFT’s Soumaya Keynes has already briefly mentioned this paper, but it’s interesting enough to warrant another take, given how it underscores how extreme levels of American partisanship can not just warp perception of the real economy, but actually affect it.

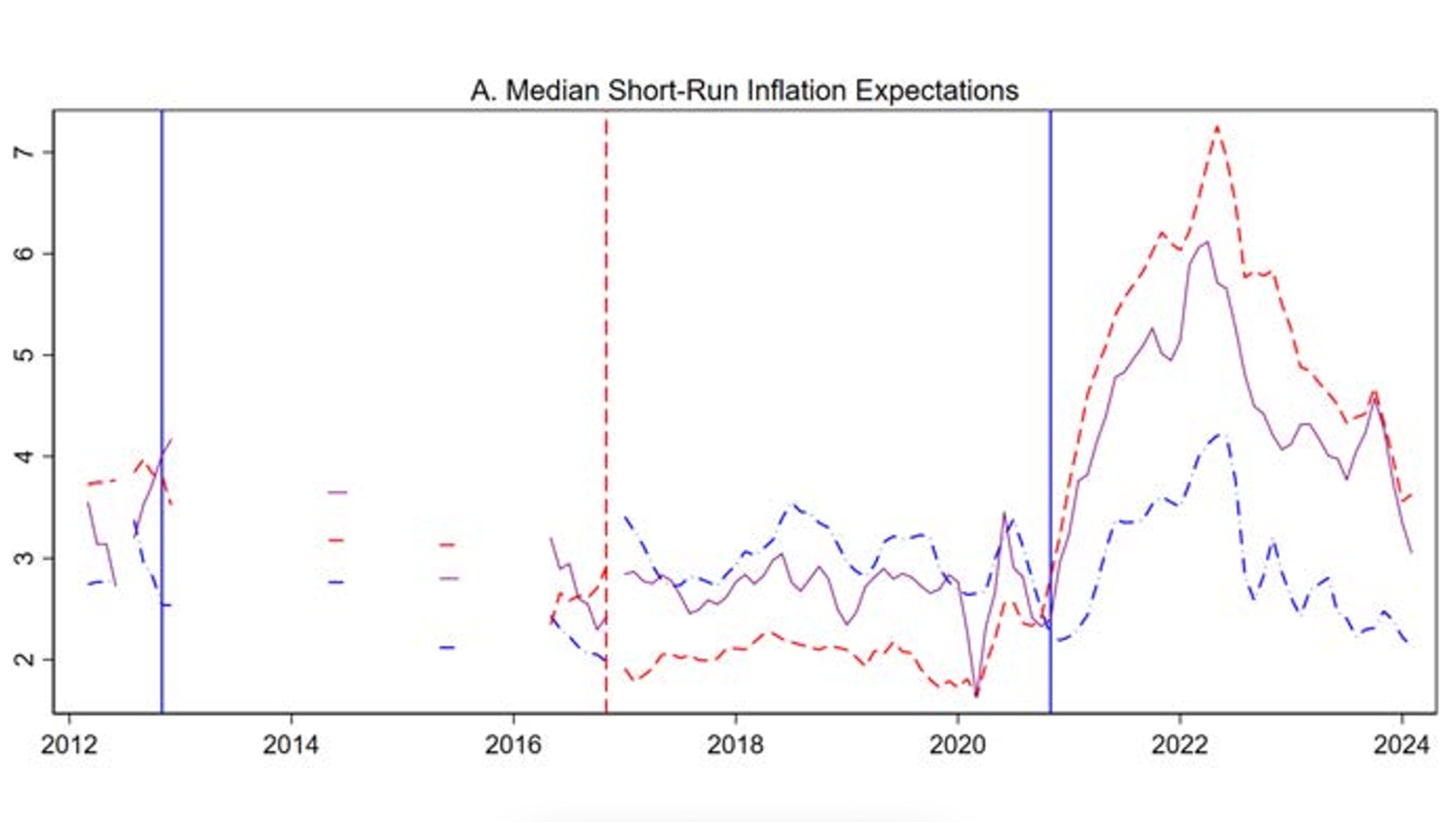

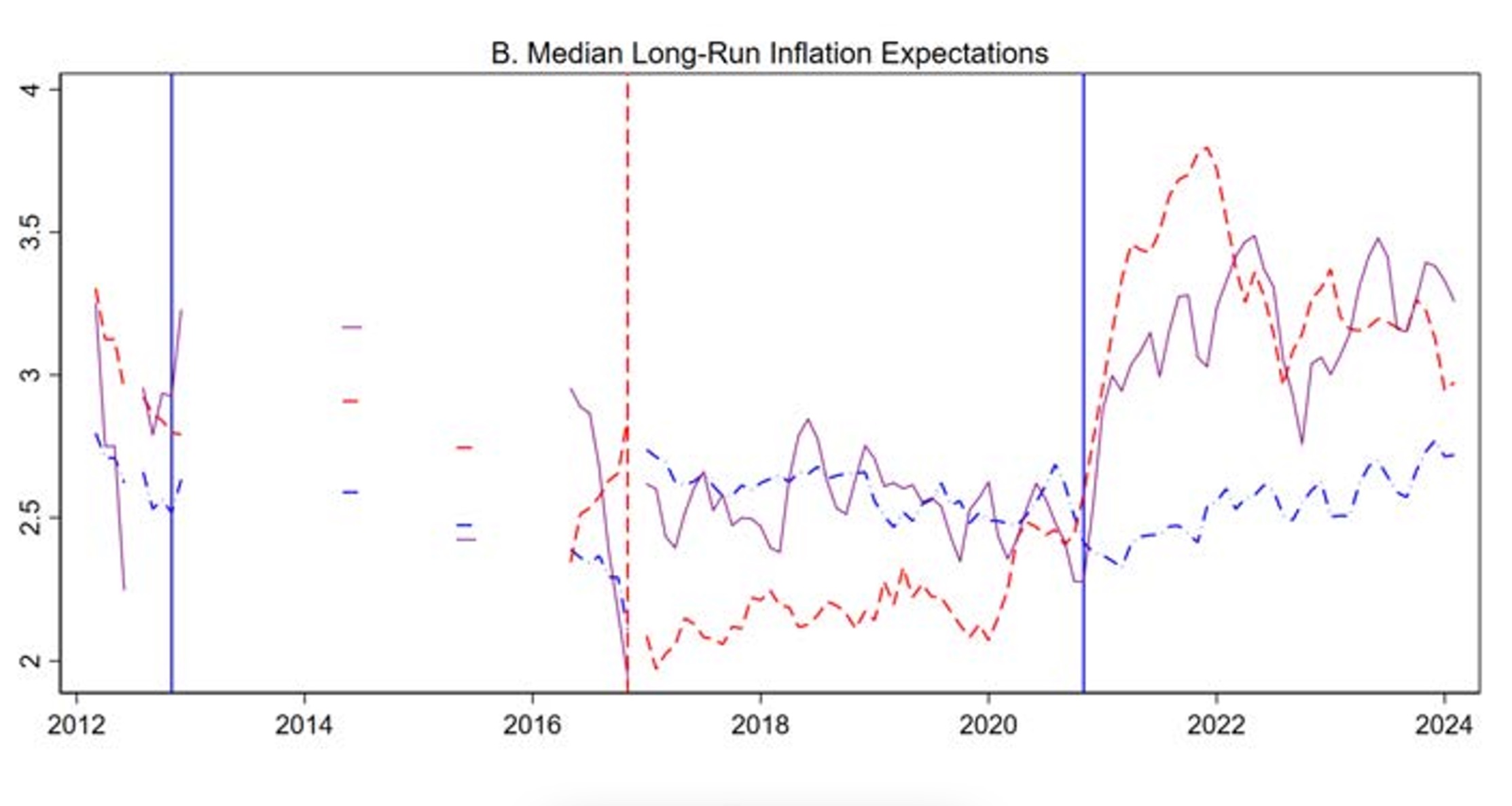

The three economists detail how Democrats’ inflation expectations remained relatively muted in the recent bout of price rises, while Republicans on average took a dourer view. In macro argot, their inflation expectations became “unanchored” from the Fed’s 2 per cent long-term inflation target.

In fact, Democrats’ expectations remained quite stable throughout the entire period from 2020 through 2023, while nearly the entire rise and subsequent fall in inflation expectations can be attributed to Republicans and Independents. The departure of Republicans’ longer-run expectations from the Federal Reserve’s two percent inflation target is not the only indication that these expectations became unanchored. Republicans also became more uncertain about longer-run inflation, and their expectations unlike Democrats’ became more responsive to inflation itself and to gas and energy prices.

Here’s what that looks like in practice, for short-term and long-term inflation expectations respectively (zoom here for the first chart, and zoom here for the second).

The vertical lines show the start of Barack Obama, Donald Trump and Joe Biden’s presidencies. The red line shows median Republican inflation expectations, while the purple and blue lines show the same for independents and Democrats respectively.

You could say that this shows that Republicans and independents were suitably and correctly sceptical of Team Transitory’s arguments. Inflation really did go higher and stay higher than the Fed and financial markets expected!

The problem is that rising inflation expectations can filter into actual inflation. When you think inflation is higher than it really is — and is going to go higher — it tends to feed into both wages and prices. This is why central banks tend to care just as much if not more about inflation expectations as they do actual month-by-month CPI reports.

Indeed, Binder, Kamdar and Ryngaert found that regions with more Republicans tended to have higher inflation — a complete reversal from the pre-pandemic trend, when inflation tended to be higher in more Democratic areas.

If non-Democrats were simply voting by survey that is, reporting high inflation expectations on the survey to express their dislike of the Biden Administration then their higher reported expectations might be a form of measurement error that does not matter for inflation. This does not seem to be the case: we find non-trivial inflationary effects from the partial de-anchoring.

From this they estimate that actual inflation would be 2-3 percentage points higher over the past few years if everyone’s expectations had become as unanchored as those of Republicans.

And conversely, if everyone had been as sanguine as Democrats, the inflation rate would now be back to the pre-pandemic level.

The solid black line shows the average realised inflation rate across US metropolitan statistical areas. The red line shows what it would probably have been if all expectations were equal to those in Republican MSAs, while the blue line shows what it might have been if countrywide expectations were the same in Democratic MSAs.

As the economists point out, the implications for monetary policy are . . . awkward.

We argue that long-run expectations depend not only on the monetary policy regime in place but also on the partisan interpretations of the monetary regime.

{kind=link}

{kind=link}

{kind=link}