Unlock the Editor’s Digest for free

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

Insurance is not supposed to be exciting. But Direct Line needs to offer some zing to its shareholders if it is to shake off the attentions of Belgium’s Ageas.

The struggling UK car insurer knocked back a second and slightly improved offer from Ageas last week. Now, much rests on what Direct Line’s brand new chief executive Adam Winslow delivers at full-year results this Thursday.

Direct Line last year scrapped its dividend, prompting a share price plunge and the departure of its then-chief executive. The sale of its brokered insurance unit last year has bolstered its balance sheet; a solid solvency position could enable capital returns. But a clear sense that it has put its pricing problems firmly behind it, plus a plan for competitive and profitable growth, are needed to see off Ageas’s efforts.

The Belgian company reinforced the idea that this is a cut-price, opportunistic bid, with a second cash-and-shares proposal of about 239p per share. That offered only a 3 per cent improvement on its first attempt. It did tweak the cash portion higher by 20 per cent. But Direct Line shareholders would still be taking half the £3.1bn value in Ageas equity.

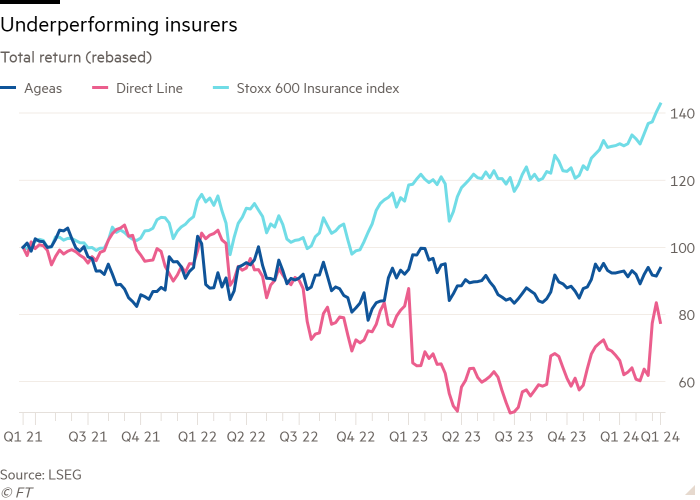

Direct Line shareholders should be wary given Ageas’s poor performance in recent years thanks to its overexposure to unfashionable guaranteed life contracts. Total returns for the group’s shares have underperformed the Stoxx 600 insurance sector by a third over the past three years. At just 6 times forward earnings, it is traded at a 50 per cent earnings discount to the same benchmark.

Its bid for Direct Line is pitched at over 10 times 2025 earnings, reason enough for Ageas investors to balk. That is in line with where Direct Line shares traded prior to 2023 but short of where anyone thinks its board will probably engage, at perhaps closer to 270p.

Still, Direct Line has yet to put up much of a defence in terms of its own outlook. Another plan to cut costs is likely on Thursday. A share buyback would reduce excess capital and the drag on the shares from last year’s divisional sale, thinks Berenberg.

Neither side in this stand-off is offering up much excitement to Direct Line’s long-suffering shareholders. But for Winslow, the above could buy him enough time to get back to the boring business of an insurance turnaround.

{kind=link}