Unlock the Editor’s Digest for free

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

Markets are sliding and the main stories investors tell themselves to understand the world are disintegrating. Apart from that, the second quarter of the year is going just great. The first of those stories, or “narratives” if you want to try and sound clever, is around the interest rate outlook. There, both policymakers and investors are putting their hands up and admitting they got this wrong. A run of upbeat inflation data means we are no longer likely to see the Federal Reserve cutting rates hard and fast, kicking one of the foundational pillars away from gains in risky asset prices. This rather embarrassing rethink on what is, after all, the biggest variable in determining how stocks and bonds behave, matters a great deal. But it is not the only market pillar that is buckling, and feeding a 4 per cent decline in global stocks so far this month.

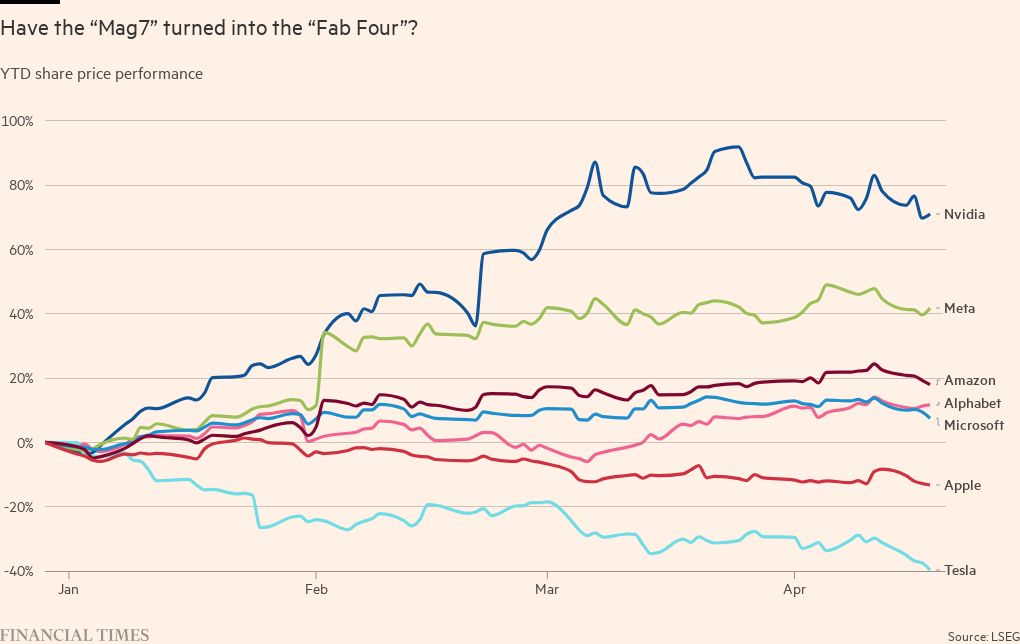

Another is the much-vaunted Magnificent Seven phenomenon, whereby a handful of supersized US tech-focused companies, particularly those with a whiff of artificial intelligence about them, have been holding up a whole lot of sky. Together, Nvidia, Meta, Apple, Tesla, Amazon, Alphabet and Microsoft, have done a huge amount of the heavy lifting in pulling up the overall US stock market — and even global stocks in recent months. They famously account for around a quarter of the value of the entire S&P 500 index of US stocks. You could fit several European stock markets inside any one of them.

This has been a perfect theme for investors for almost a year. Catchy nickname? Check. Eye-popping numbers? Check. Gigantic returns for investors who got in before the latest sweep higher? Sure. If you bought stocks in chipmaker Nvidia at the start of this year, you are up a cool 70 per cent or so. Nice work if you can get it. Plenty of other markets in Europe and Asia have much higher levels of concentration. But the vast size of these US companies — Nvidia’s market capitalisation is around $2tn — means they are often cited not just as a collection of stocks but as a determinant of where other asset prices head too.

The problem is that even Nvidia has come off the boil, despite posting blowout earnings figures earlier this year. From the high point in early March, the stock is down 12 per cent. Tesla shares are a horror show, down 40 per cent so far in 2024. Apple has shed 13 per cent. Microsoft is up “just” 7 per cent or so — still extremely respectable of course but it has cooled so far in April. Amazon is up 18 per cent and Meta has gained 42 per cent. Google is up 12.

Enquiring minds have to ask whether the “Mag7” is a cohesive theme at all or just a handy moniker — even a joke that went too far, dreamt up by investment banks (probably) or journalists (no, definitely not). New variants doing the rounds include the Fab Four or even the Terrific Two and Floppy Five. Never underestimate the propensity of the supposedly-very-serious financial services industry to come up with this stuff. (It’s worth stressing that, as we’ve pointed out before, the thing with the Magnificent Seven in the film that inspired the name, is that four of the seven heroes are dead by the end.)

Fund managers now have to decide whether the latest downdraft in these stocks is something to fear or just a blip. Has the excitement around AI-flavoured stocks simply run ahead of itself? Does it make sense to reward the creators and early users of AI technology rather than stocks in healthcare, banking or whatever sectors are likely to be the long-term beneficiaries?

Yves Choueifaty, founder of French investment house Tobam and a true believer in the power of portfolio diversification, said the degree of market concentration embedded in these stocks is unhealthy. “Have we reached the maximum? Nobody knows,” he said. “Everybody knows this concentration is not sustainable over the long term, but it can still continue for a few months or even a couple of years.”

But a new note from HSBC suggests this trend may be just getting going. “To truly understand how dominant they have been, consider that only 5 per cent of the market — around 25 stocks — has delivered stronger returns on a year-on-year basis,” wrote global equity strategist Alastair Pinder. But “the real surprise” is that the bank’s survey of 150 of the largest US funds shows “nearly every US fund manager is underweight these stocks collectively” due to restrictions for some types of funds on single-stock concentration.

“All of the Magnificent 7 rank in the top 10 largest fund underweights relative to the benchmark,” he wrote, with Apple top of the pile. “One could argue that the Magnificent 7 are simultaneously the most over-owned and most underweight stocks in the US.” Some big mutual fund managers have already started reclassifying funds to free them from position limits. HSBC thinks this is likely to continue and could push further investment in the direction of this group — although one imagines some will now steer clear of Tesla.

The mood among fund managers still appears to be an inclination to buy dips, and this is the first dip in key stocks indices that we have seen for some months. It’s a test of nerve nonetheless, with few guiding lights to rely on.

katie.martin@ft.com

{kind=link}