Unlock the Editor’s Digest for free

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

A Marks and Spencer superapp would be catnip for investors and Middle England alike. Little wonder that a report claiming it was on the cards sparked the odd frisson.

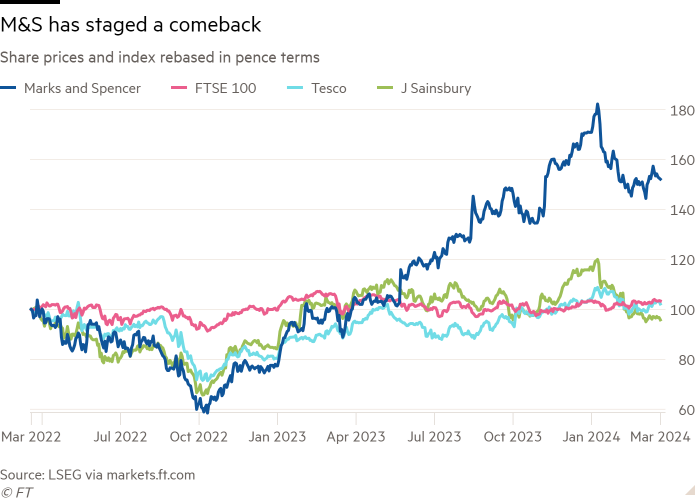

As purveyor of the nation’s undies and groceries, M&S is a British institution. It is also a Great British comeback story. Once dismissed for its lacklustre clothing and still more lacklustre financial performance, the retailer is staging a turnaround under Stuart Machin, who took the reins just under two years ago.

Machin’s “M&S Reshaped” strategy, including cost cutting and streamlining supply chains, has already produced results. Like-for-like food sales rose 9.9 per cent in the most recent third quarter; clothing and homeware was up 4.8 per cent on the same basis.

Investors rewarded the group with an almost 70 per cent rise in the share price over the past 12 months, vastly outpacing peers J Sainsbury and Tesco. During this period the benchmark FTSE 100, to which M&S was last year readmitted after a four-year hiatus, has barely budged.

M&S has also diverged from rivals by sticking with financial services, a sector supermarkets rushed into in the 1990s, counting on their brands to hoover up market share. That didn’t pan out as envisioned: Tesco and Sainsbury have both staged retreats this year.

Machin is barely two years into a five-year plan that aims to lift market share, profits and operating margins. Digital, including data and IT, is one area where much of the reshaping is yet to come — now under Rachel Higham following Katie Bickerstaffe’s departure. Among other steps, M&S wants to enhance the app and double its 5mn or so users in two years.

Adding digital payments to the mix is the sine qua non of any superapp, encouraging usage, providing a wealth of customer data and more scope for monetisation. It is also one of the toughest propositions, as Meta, among others, have discovered. The social media group’s WhatsApp Pay is only available in Brazil, India and Singapore.

That underlines the chasm between superapp ambition and actuality. Despite big talk — Elon Musk is among those flagging superapp plans — no operator outside Asia has succeeded in pulling off an all-encompassing app that lets you pay, play, shop and work.

Uber has tempered its ambitions to become more of a travel and delivery app. Fintech Revolut is taking small steps, having added apps for messaging (Revolut Chat) and booking trips (Revolut Stays).

Chinese superapps began earlier and are far more embedded into the fabric of daily life, wrapping in messaging, finance, shopping, gaming and almost anything else. But the terrain is kinder: scant foreign competition, a domestic market of 1.4bn and preponderance of merchants that only accept payment by app.

It is also hard to achieve the network effect enjoyed by Tencent and Alibaba, the tech groups behind China’s biggest superapps. Even if Machin succeeds in lifting M&S’s market share by 1 percentage point, it will still have under 5 per cent of the UK grocer market.

That is not to say a spruced-up app is a dud. M&S’s contract with HSBC, which owns M&S Bank, is up for renewal. M&S is likely to push for more control and a bigger cut of the spoils.

Enabling shopping and payment within a single app is easier for customers, which should ultimately pay off for the retailer too. Not super maybe, but certainly good.

Food for thought at Unilever

Spin-offs work particularly well when the original corporate hodge podge obscures the value of one (or more) true gems. That isn’t the case with Unilever’s proposed demerger of its ice-cream business.

Instead of an uplift in valuation, the scoop-out may simply increase investor appetite for bolder action on the group’s bloated portfolio.

Unilever’s plan is best understood as the unwinding of a corporate footprint which made little sense in the first place. Ice-cream — which accounted for 13 per cent of Unilever’s total sales last year — has few synergies with the rest of the group’s home, food and personal care business. It is more capital intensive and volatile, with lower operating margins of 10.8 per cent in 2023, compared with 16.7 per cent for Unilever as a whole.

Yet scooping out the division will not — of itself — unlock value for Unilever’s shareholders. Imagine that the new ice-cream company traded in line with the valuation at which Nestlé sold Häagen-Dazs in 2019, and lop the resulting €17bn (£14.5bn) off Unilever’s current £118bn of enterprise value. That would leave the rump trading at 12.8 times forward ebit. That’s cheaper, but not miles away, from its current multiple of 13.4 times.

Such back-of-the envelope maths implies that financial engineering alone won’t cut the mustard. Unilever will need to improve its core business — comprising condiments such as Hellmann’s and Knorr, and cleaning products Cif and Domestos — if it is to narrow its valuation gap with peers.

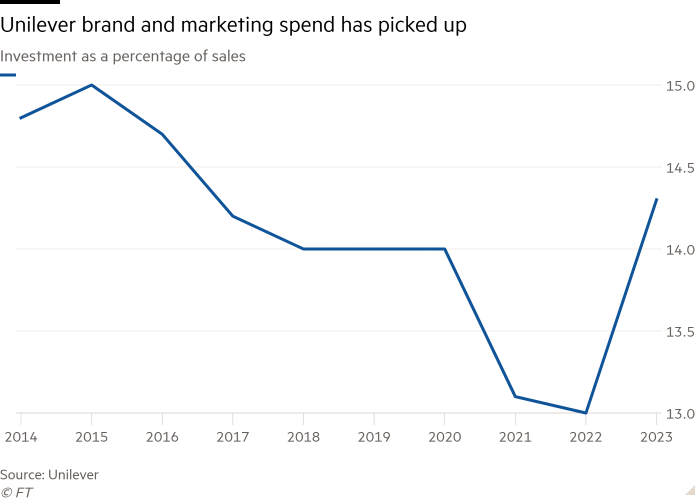

New boss Hein Schumacher basically plans to run a tighter ship. He has nudged up growth targets, from the current 3-5 per cent to “mid single digits”, and announced £800mn of cost cuts. A smidgen comes from shedding lower growth ice-cream. The rest, one hopes, will come from new investment. Brand and marketing spending is on the up: from 13 per cent of sales in 2022 to 14.3 per cent last year. The cost cuts will create space for more.

The snag is that investors have been here before. Actually making the announced cost cuts and reinvesting the money profitably requires better execution than Unilever has managed in the past. Schumacher reckons the demerger will help by reducing complexity, improving focus and speeding decision making.

If that really is the case, shareholders may soon be clamouring for Unilever’s management to hive off its food business and give the potentially higher-growth home and personal care segment their undivided attention.

{kind=link}