Stay informed with free updates

Simply sign up to the Chinese business & finance myFT Digest — delivered directly to your inbox.

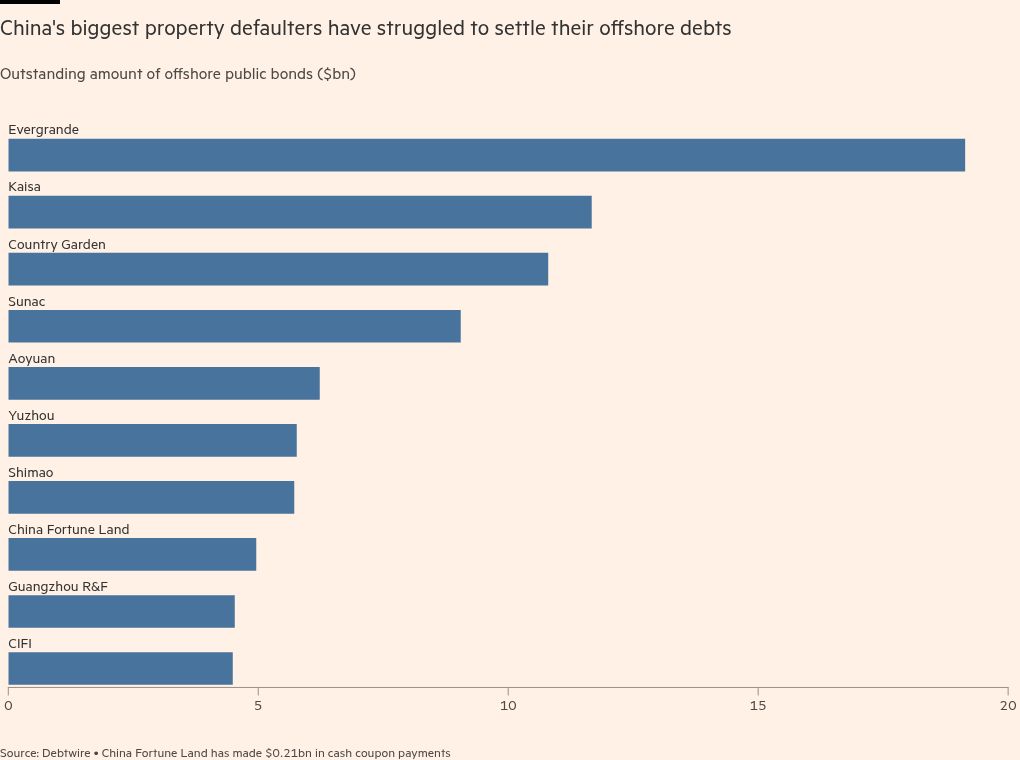

International bondholders have recovered less than 1 per cent of nearly $150bn of bonds defaulted on by China’s property developers since 2021, despite years of negotiations and nearly a dozen restructuring agreements.

Just $917mn in cash has been transferred to investors in offshore bonds across 62 developers in that period, according to an analysis of restructuring data from Debtwire, equivalent to 0.6 per cent of the $147bn in defaults recorded.

Only three developers — China Fortune Land Development, China South City and RiseSun Real Estate Development — have made any cash coupon payments across 11 restructuring agreements for $39bn in debt, as mainland property businesses struggle to generate income.

The data highlights the difficulties for international investors in recovering money from any of their holdings in Chinese developers, which borrowed heavily on overseas markets during a boom that unravelled following the default of Evergrande in 2021.

It also casts doubt over the viability of a host of restructuring agreements forged in Hong Kong and illustrates the depth of China’s property market slowdown, despite government efforts to restore confidence, including cutting interest rates and completing unfinished projects.

A restructuring adviser in Hong Kong, who did not wish to be named, said he was not aware of any cash moving from mainland developers to outside the country because of their ongoing difficulties.

“Everyone’s just thrown in the towel,” said Debtwire analyst Dominic Soon. “The main problem is really the onshore debt. Without solving that, there’s almost no money that can come out.”

The offshore bonds are dwarfed by debts in the mainland, which pose a much graver challenge to policymakers as they seek to stabilise an economically critical sector. Total developer liabilities were $12tn, according to a 2023 estimate by the National Bureau of Statistics.

Debtwire’s Soon suggested restructuring developments in the mainland were lagging those in Hong Kong by several years.

A handful of Chinese developers listed in Hong Kong, including Evergrande, face winding-up petitions in the city. But almost all of their operations are in mainland China, governed by a separate legal code, and there is little evidence of liquidation proceedings affecting their operations at home.

Instead, the process has overwhelmingly focused on recouping value from offshore assets owned by the companies, as well as restructuring deals that rely on mainland cash flows eventually recovering in several years’ time.

Offshore debts have received heightened investor focus because of more transparent default procedures governing international bonds. However, Evergrande, the most indebted developer globally, with about $340bn in liabilities according to its most recent disclosures, borrowed only $20bn offshore.

According to the Debtwire analysis, of the $917mn paid so far, about $200mn came in consent fees paid to investors to secure the deals, while $30mn was paid to ad hoc creditor groups. The data company assumes required cash payments were made unless public information indicates otherwise.

Chinese developer Sunac unveiled an offshore restructuring in late 2023 that bolstered hopes of recovery for bondholders. But this week, it said it would start the process again after warning it would struggle to make offshore payments.

Sunac, which faces a winding-up petition in Hong Kong, did not respond to a request for comment.

National Bureau of Statistics data released last week showed total property development investment fell 10 per cent in the first two months of 2025 compared with the same period last year, while new home prices in the 70 biggest cities declined month on month in February.

Additional reporting by Wang Xueqiao in Shanghai and data visualisation by Haohsiang Ko

{kind=link}