ArLawKa AungTun/iStock via Getty Images

Real estate stocks ended the week in green after three consecutive weeks of decline, as analysts turned positive as well as the sector delivered strong earnings, even amid dim chances of a near-term rate cut.

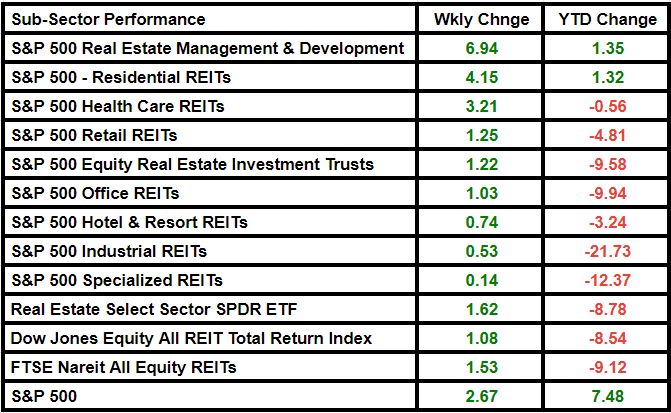

Real Estate Select Sector SPDR ETF (NYSEARCA:XLRE) closed 1.62% higher at 36.46, although underperforming the broader S&P 500 index, which rose 2.67% comparatively.

The Dow Jones Equity All REIT Total Return Index was up 1.08%, while the FTSE Nareit All Equity REITs index increased by 1.53%.

The Core PCE Price Index, the Federal Reserve’s preferred measure of underlying inflation, rose in line with consensus in March. Investors pushed back their rate cut expectations in reaction to the latest data on the U.S. economy, which indicated that GDP only grew at an annual rate of 1.6% in the first quarter, well below the 2.2% consensus forecast. Now, the consensus is that the first 25 basis points rate cut will take place in December.

However, analysts showed optimism in the real estate stocks this week. UDR (UDR) was upgraded at UBS on increasing confidence in its rent growth trajectory at a favorable valuation. Mizhuo Securities resumed coverage of Healthpeak Properties (DOC) with a Buy rating on the back of its merger with Physicians Realty.

Deutsche Bank upgraded Federal Realty Investment Trust (FRT), considering that recent office lease announcements should assuage investors’ concerns about the office part of the REIT’s mixed-use properties.

Equity Residential (EQR) was upgraded by BMO Capital Markets ahead of its earnings results. Multifamily REITs, including EQR, are changing hands at discounted valuations, “largely due to supply concerns in the Sunbelt,” analyst John Kim wrote in a note. However, BMO downgraded Prologis (PLD) as Kim sees “the shares as being under pressure as long as the demand picture remains murky.”

Seeking Alpha’s Quant Rating system changed its rating on XLRE to Sell from Strong Sell this week, with a score of 1.78 on a scale of 5. SA analysts continue to grade the ETF as a Buy.

Earnings:

This week saw some big real estate names deliver solid earnings growth, which continued to demonstrate the sector’s disciplined balance sheet.

Alexandria Real Estate Equities (ARE) closed 2.49% higher on Monday after posting earnings and revenue that exceeded the average analyst estimate as expenses fell markedly. Equity Residential (EQR) rose 1.3% in Tuesday after-hours trading after Q1 results. CoStar Group (CSGP) was positively impacted by a Q1 beat as well as the Matterport deal, particularly closing the day after its results’ announcement 8.66% higher.

Healthpeak Properties (DOC) closed Friday 2.51% higher after posting a beat and 2024 guidance boost on Thursday after market hours. The case was the same for AvalonBay Communities (AVB), with the stock closing marginally higher on Friday. Weyerhaeuser (WY) posted on Thursday Q1 earnings that came in slightly above the Wall Street consensus, but fell markedly both sequentially and from a year ago.

WY was among the worst-performing S&P 500 real estate stocks this week, along with Equinix (EQIX), Crown Castle (CCI), Public Storage(PSA) and Regency Centers (REG). CSGP, EQR and DOC were among the best performing stocks, along with Essex Property Trust (ESS) and Digital Realty Trust (DLR). reAlpha Tech (AIRE), Braemar Hotels & Resorts (BHR), Altisource Portfolio Solutions (ASPS), KE Holdings (BEKE) and Ohmyhome (OMH) were among the other major real estate names that delivered positive returns during the week.

Major real estate names expected to report next week include W. P. Carey (WPC), American Tower (AMT), Omega Healthcare Investors (OHI), Iron Mountain (IRM), VICI Properties (VICI) and STAG Industrial (STAG), among others.

Fund Flows:

Funds continued to flow out from The Real Estate Select Sector SPDR Fund ETF this week, demonstrating bearish investor sentiment.

XLRE saw net outflows of ~$40.05M, compared to outflows of ~$36.26M last week, according to the data solutions provider VettaFi.

Optimism about the short-term outlook for the broader stock market continued to decline, as steady inflation and a flurry of earnings report from key players weighed on investors’ sentiment.

Subsector Performance:

Real Estate Management & Development and Residential REITs were the notable winners among subsectors.

The strength of the residential subsector was particularly evident in the March home sales report, which showed that new home sales jumped past consensus during the month. The purchase demand remains steady even as mortgage rates continued to rise.

Here is a look at the subsector performance:

{kind=link}