Stay informed with free updates

Simply sign up to the Property sector myFT Digest — delivered directly to your inbox.

The Federal Reserve might not have actually cut interest rates yet, but as far as US housing is concerned, the fabled pivot has already started. And it’s seismic.

With the 30-year Treasury yield sliding from a high of over 5 per cent last October to nearly 4 per cent this month, US mortgage rates have tumbled from nearly 8 per cent to about 6.5 per cent.

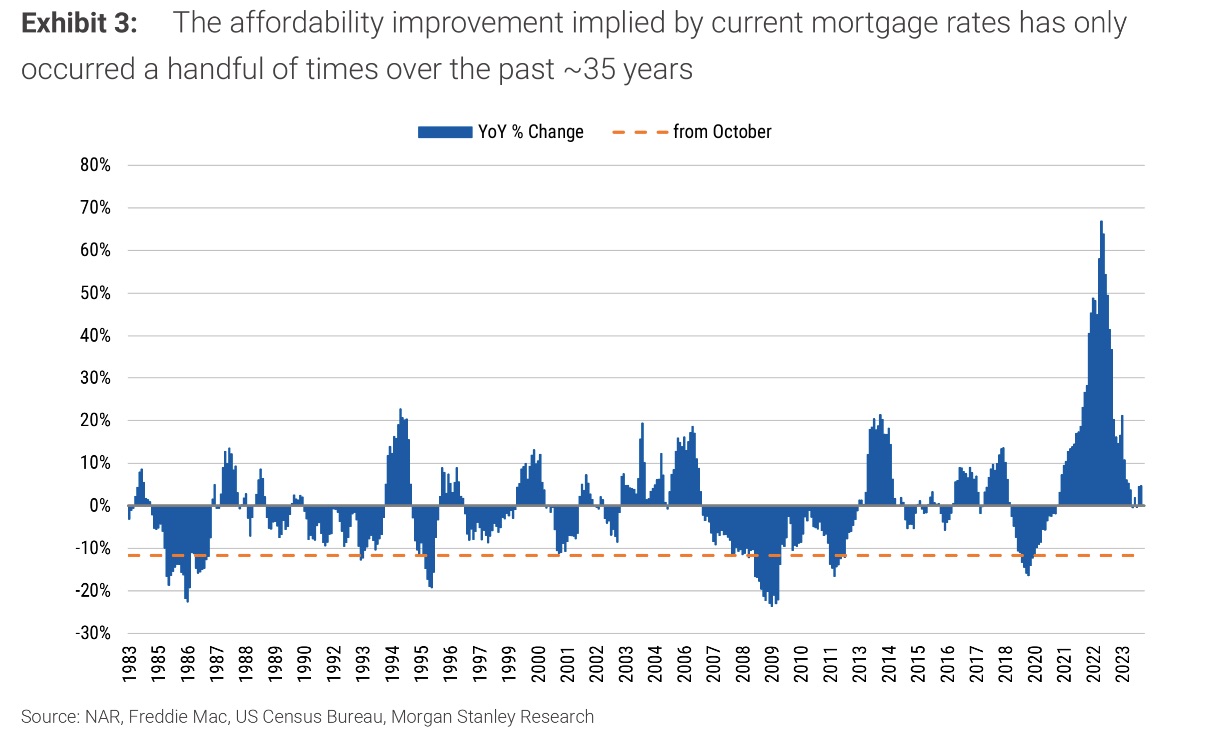

That is one of the biggest improvements in affordability in the past four decades, according to Morgan Stanley, and probably the biggest mortgage rate whiplash in history (zoomable version):

So what does this mean for the weird, comatose US housing market?

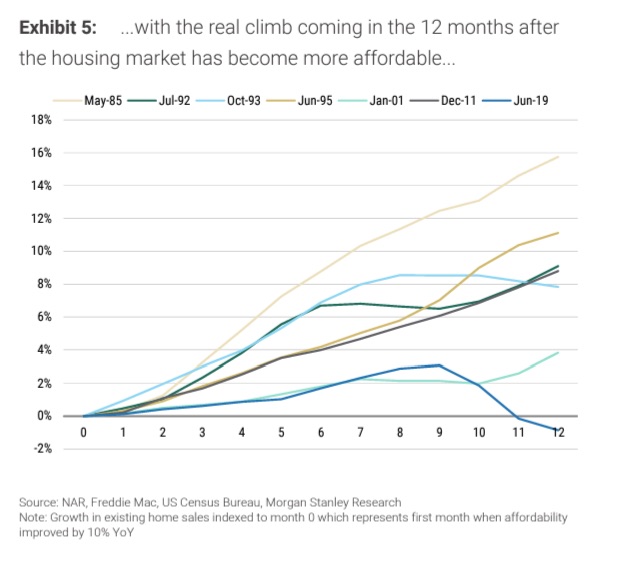

Morgan Stanley looked at the other time when affordability improved by 10 percentage points or more, and found that home sales tend to remain sluggish for a while, before picking up briskly over the next 12–24 months.

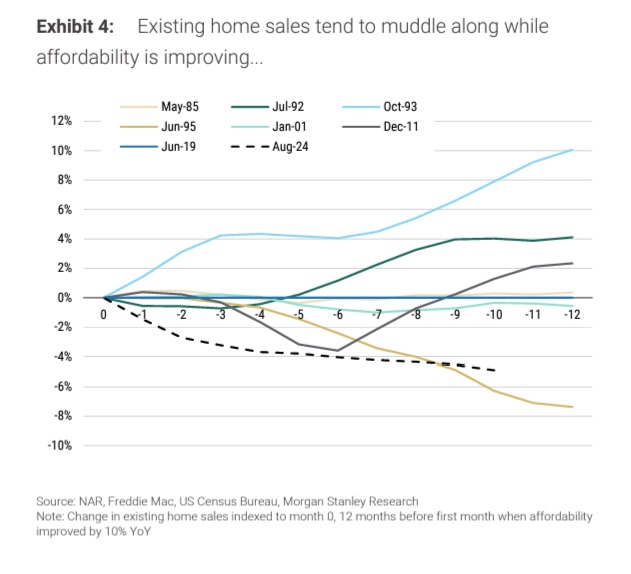

(Left and right zoomable versions.)

However, as you can see from the above chart to the left, we’re currently tracking considerably below the norm.

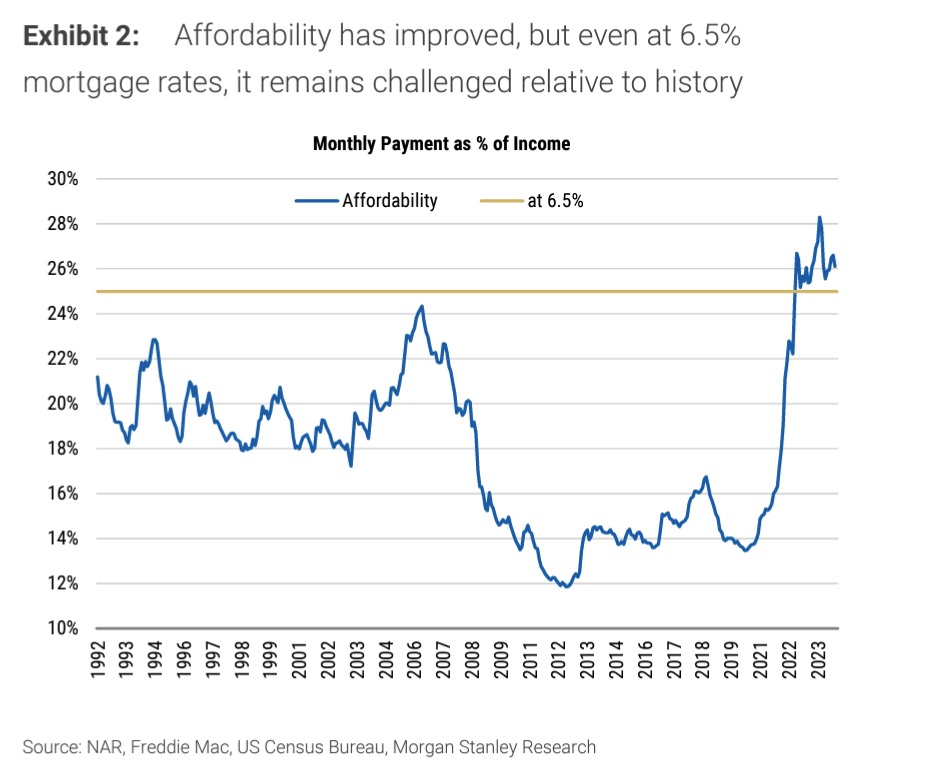

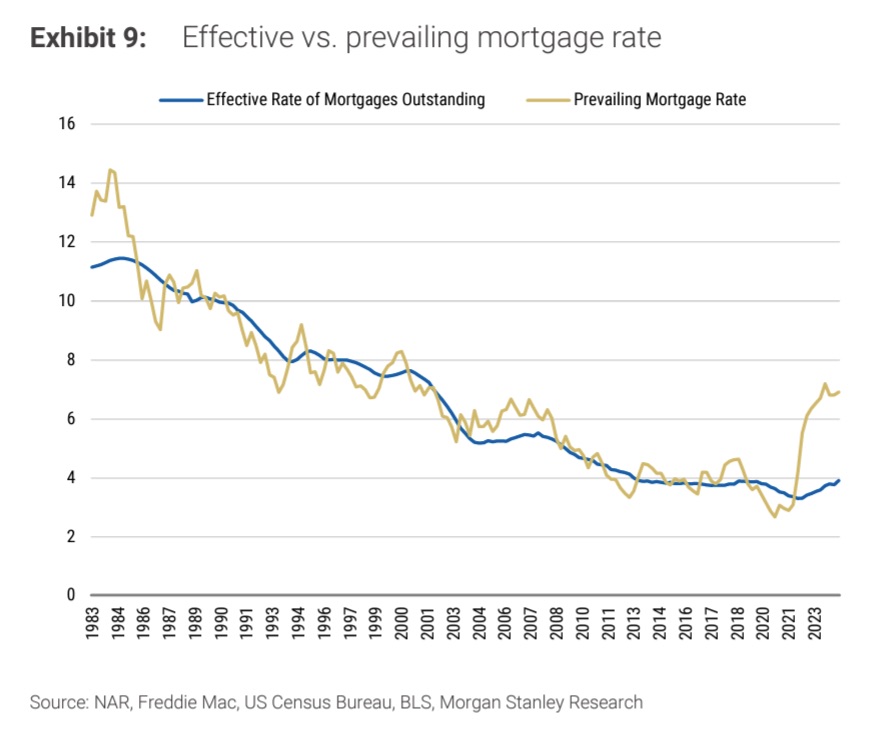

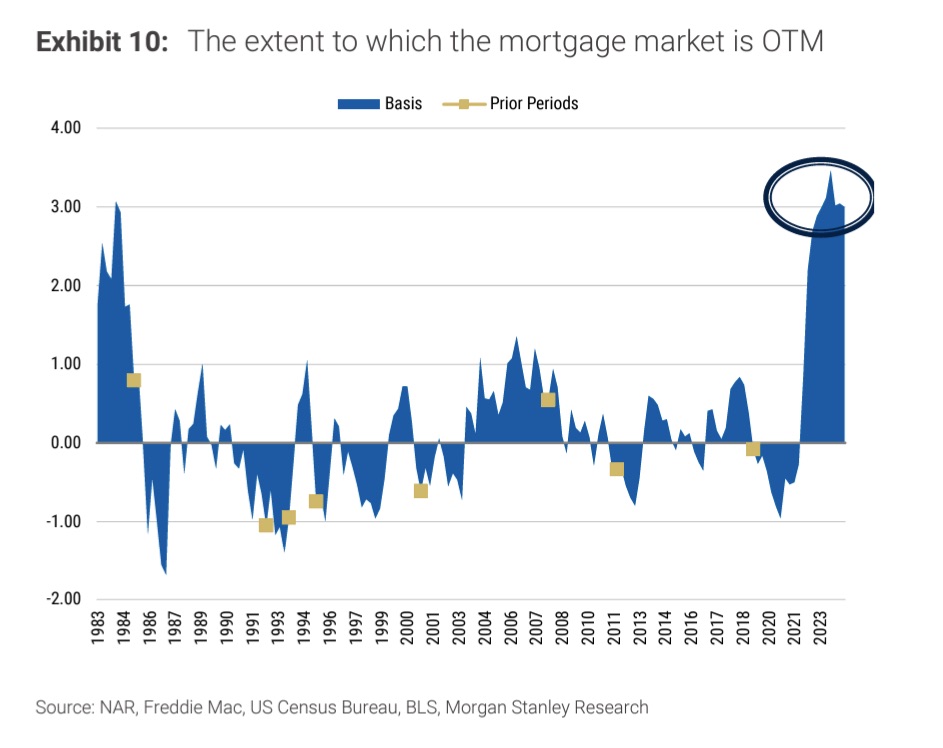

That’s almost certainly because the affordability of US mortgages remains pretty bad even after the recent improvement (zoomable version):

If you’re living in a house with a long term fixed rate mortgage that costs 3-4 per cent, moving and resetting to over 6 per cent is still a big ask, even if it is not as bad as resetting to 7–8 per cent.

And Morgan Stanley estimates that the gap between the current mortgage rate and what the average US household is currently actually paying for their mortgage is the greatest since at least the early 1980s.

Which is why the US housing market will probably remain in near-stasis until the classic 30-year fixed mortgage rate drop a LOT lower. As Morgan Stanley’s economists conclude:

When looking exclusively at prior periods of significant affordability improvement, it would seem to suggest that existing home sales could increase at a healthy clip in the next couple of years. However, upon a closer look at the overlapping narratives concerning the extent to which homeowners are locked in, how unaffordable the housing market is today, and how few homes are available for sale, it seems that existing home sales volumes are fighting more of an uphill battle today.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}