Damircudic | E+ | Getty Images

The tax deadline is approaching and there’s still time to score a deduction with a pretax individual retirement account contribution — if you qualify.

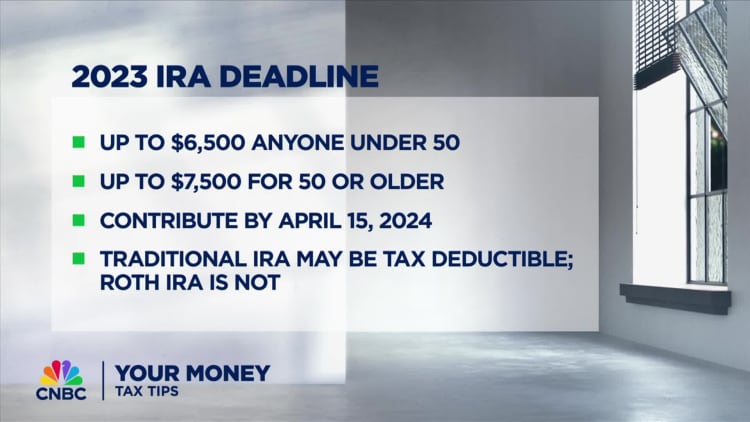

For 2023, the IRA contribution limit was $6,500, plus an extra $1,000 for investors age 50 and older. That increased to $7,000 for 2024, with $1,000 more for catch-up contributions.

You can still add money to your IRA for 2023 before the federal tax deadline, which is April 15 for most taxpayers. But you must designate the deposit for tax year 2023.

More from Personal Finance:

There’s still time to reduce your tax bill or boost your refund before the deadline

An ‘often overlooked’ retirement savings option can lower your tax bill

Some retirement savers can still get a ‘special tax credit,’ IRS says

A last minute pretax IRA contribution for 2023 could qualify for an “above-the-line” deduction, which you can claim even if you don’t itemize tax breaks, and it reduces your adjusted gross income.

However, the IRA deductibility rules can be “very confusing,” according to Mark Steber, chief tax information officer at Jackson Hewitt.

Your eligibility for a pretax IRA deduction depends on three factors: your filing status, modified adjusted gross income and your workplace retirement plan.

Here’s who qualifies for the IRA deduction

If you don’t have a workplace retirement plan, there’s no income limit for IRA deductions, which could be appealing for higher earners, experts say.

But it’s more complicated if you participate in a workplace retirement plan. “Participation” could include employee contributions, company matches, profit-sharing or other employer deposits.

“It’s important to understand there are deductibility limitations,” certified financial planner Malcolm Ethridge, executive vice president of CIC Wealth in Rockville, Maryland, recently told CNBC.

You could deduct all, part, or none of your pretax IRA contributions, depending on your filing status and income. The complete IRS eligibility chart is available here.

For 2023, there’s a full deduction for single filers with a modified adjusted gross income of $73,000 or less, and a partial deduction up to $83,000.

The limits are higher for married couples filing together, with a full deduction at $116,000 or less, and a partial deduction before reaching $136,000.

“Even if you maxed out the plan at your current company, your income could still be low enough to make a tax-deductible [IRA] contribution,” Ethridge said.

Consider your investing goals first

While scoring a last minute deduction with a pretax contribution may be tempting, you need to consider your goals and timeline before proceeding, experts say.

The contribution could offer a benefit this year, only to create a future “tax problem,” said CFP Laura Mattia, CEO of Atlas Fiduciary Financial in Sarasota, Florida.

Plus, you need to weigh your immediate priorities, including major expenses, because “you don’t want to use a retirement vehicle for shorter-term savings,” she said.

{kind=link}