Stay informed with free updates

Simply sign up to the US inflation myFT Digest — delivered directly to your inbox.

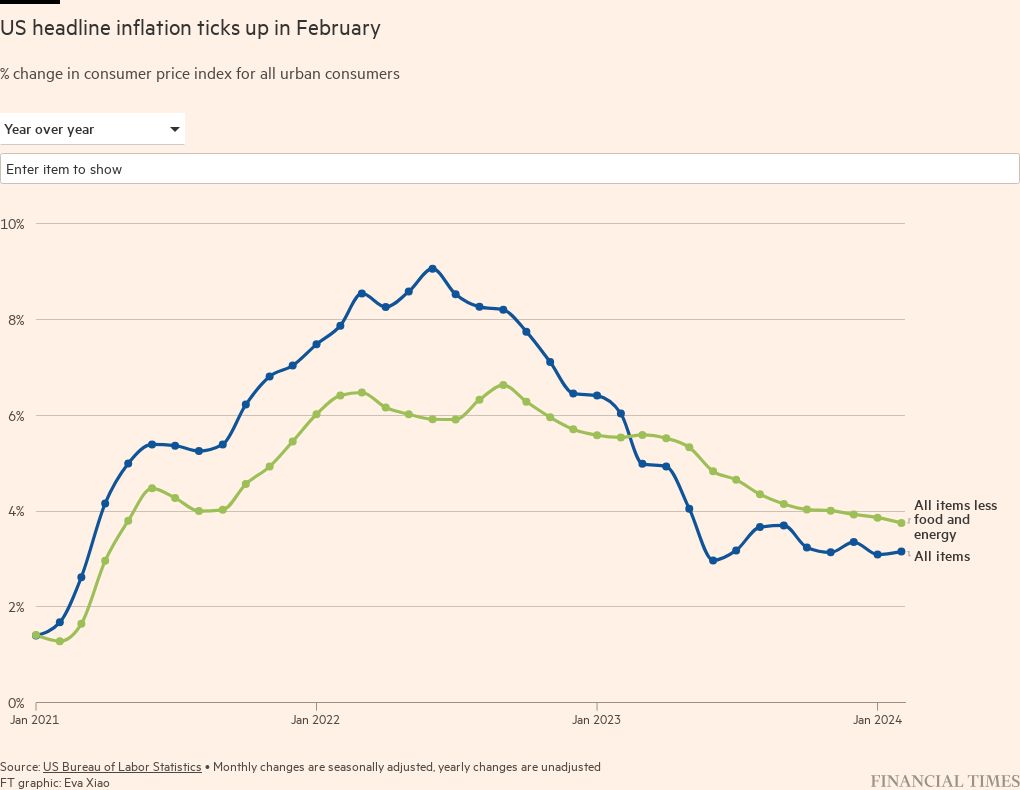

US inflation unexpectedly increased to 3.2 per cent last month, highlighting the challenge faced by the Federal Reserve in the “last mile” of its fight against rising prices.

Economists polled by Bloomberg had expected annual consumer price inflation to remain unchanged from January’s rate of 3.1 per cent.

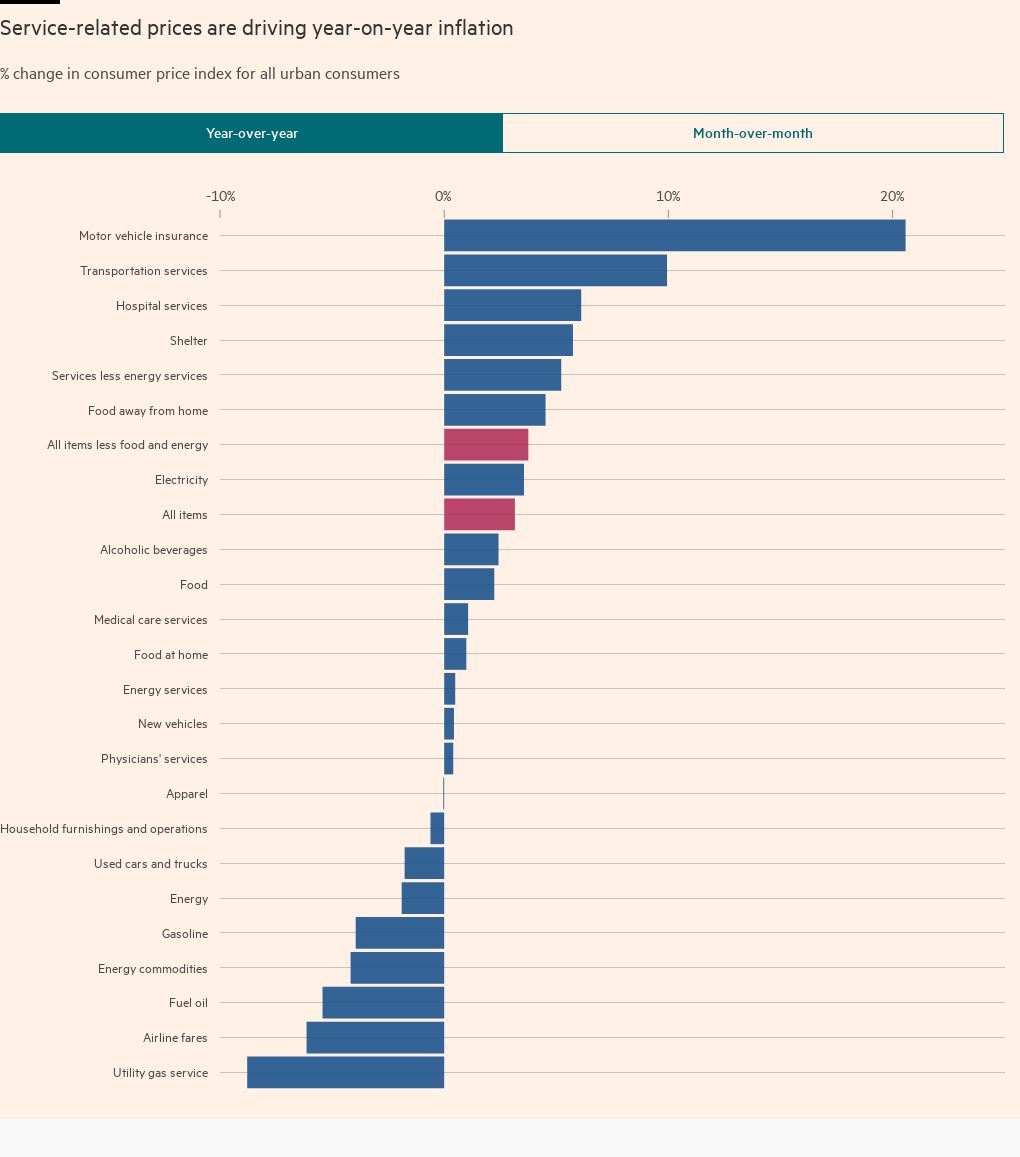

But Tuesday’s rise, largely stoked by services such as motor insurance and health, triggered warnings that the Fed may have to wait longer than previously expected before cutting interest rates from their current 23-year high.

“These inflation numbers presage a rockier period ahead for the Fed,” said Eswar Prasad, a professor at Cornell University.

“Although the US economy has held up well so far, there is a risk that persistent inflation and the Fed’s response to it might turn a soft landing scenario into a soft stagflation one.”

Tuesday’s figures will play an important part in the Fed’s thinking when it publishes new projections next week on how many cuts it expects for 2024. The March 20 meeting is also expected to keep rates at between 5.25 and 5.5 per cent.

Diane Swonk, chief economist at KPMG US, suggested the inflation data would bolster the resolve of hawks at the central bank who want to keep rates higher for longer to get inflation back to its 2 per cent target.

“It’s going to be a very heated March meeting,” she said.

At present, the central bank plans to reduce rates three times this year. Markets expect three or four cuts this year, beginning in June or July.

“The Fed is probably still on track to cut in June,” said Citi economist Andrew Hollenhorst, who added “the last two months of inflation data show the difficulty in returning inflation to target”.

Interest rate and inflation movements are a key concern for President Joe Biden, who is seeking to make his stewardship of the economy a centrepiece of his campaign against Donald Trump, who he is lagging behind in the polls ahead of November’s election.

On Tuesday the president attacked Republicans for having “no plan to lower costs”, highlighting his own promise to tackle corporate price gouging.

Government bond prices fell slightly as investors adjusted their bets on when Fed interest rate cuts would arrive. Two-year Treasury yields, which often track rate expectations and move inversely to prices, rose 0.06 percentage points to 4.59 per cent.

The benchmark 10-year yield also added 0.05 percentage points to 4.15 per cent.

An index tracking the dollar against a basket of six other currencies was up 0.2 per cent on the day.

US stocks finished higher on Tuesday, with Wall Street’s S&P 500 climbing 1.1 per cent to a record high close and the technology-heavy Nasdaq Composite gaining 1.5 per cent.

“It’s surprising that we haven’t seen more of a negative reaction,” said Tim Murray at T Rowe Price, an asset manager. “This last mile of inflation — getting from 3 per cent to 2 per cent — is going to be really hard. Much harder than getting from 9 to 3 per cent.”

He added that the market’s hope for interest rate cuts “keeps getting pushed back . . . You have to wonder even how many cuts we’re ultimately going to get.”

But Wylie Tollette, chief investment officer at Franklin Templeton Investment Solutions, said Tuesday’s inflation reading was “just about perfect for sustaining the market rally, as it’s not too hot [and] not too cold”.

The consumer price index figures from the Bureau of Labor Statistics showed core inflation, which excludes changes in food and energy costs, at 3.8 per cent compared with 3.9 per cent in January. Economists had expected a fall in the metric, which is seen as a better measure of underlying price pressures, to 3.7 per cent.

The month-on-month headline figure rose from 0.3 per cent in January to 0.4 per cent last month.

The Fed targets an alternative measure of inflation — personal consumption expenditures. However, with the February PCE figure not being released until after the March 20 vote, the CPI data is expected to influence rate-setters’ deliberations.

{kind=link}